Most Australian fuel cards are designed for businesses, not everyday drivers, so eligibility usually comes down to having an ABN, some trading history, and the ability to pass a basic credit or risk check.

The good news is you don’t need a big fleet to qualify; even sole traders and side‑hustlers with one vehicle can usually get approved if they meet the basics.

Who can get a fuel card in Australia?

In Australia, traditional fuel cards are issued to businesses and business‑like entities, not private individuals filling up the family car. If you want a Shell Card, FleetCard, WEX Motorpass, BP Plus, 7‑Eleven Fuel Card, AmpolCard, United Card or similar, you’ll almost always need an active Australian Business Number (ABN).

Eligible customers typically include:

- Sole traders and freelancers (including side‑hustles)

- Small businesses with one or a handful of vehicles

- Medium and large fleets with cars, utes, vans or trucks

- Not‑for‑profits and some government or community organisations

If you don’t have an ABN, you generally won’t qualify for a business fuel card and may need to look at alternatives like rewards credit cards, in‑app fuel discounts or prepaid options instead.

Core eligibility requirements (across most fuel cards)

Every provider has its own application form and risk model, but the fundamentals look very similar across the main cards. Most mainstream fuel cards will expect:

- An active ABN: This is the big non‑negotiable for business fuel cards in Australia.

- A real business or commercial purpose: The fuel card must be used for business‑related vehicle expenses, not purely personal driving.

- Applicant over 18: Directors, owners or authorised signatories need to be adults able to enter a credit contract.

- Basic identity and business checks: Providers verify the ABN, business details and the applicant’s ID to reduce fraud and ensure they know who they’re lending to.

Some cards also ask for:

- A minimum trading history (often 6–12 months for unsecured accounts)

- Simple financial documents (like recent bank statements) for brand‑new or higher‑risk businesses

Sole traders and self‑employed: are you eligible?

Sole traders are one of the biggest growth segments for fuel cards – and the requirements are usually simpler than many people expect.

If you’re self‑employed, you’re typically eligible if:

- You hold a valid ABN in your own name as a sole trader.

- You use your vehicle for business (client visits, deliveries, site work, rideshare, etc.).

- You are comfortable with a basic credit check or providing some recent bank data if requested.

Many providers openly promote that you do not need a company structure or multiple vehicles; one car and a genuine business purpose is enough. For example, Shell Card and similar products explicitly state that it doesn’t matter if you have one vehicle or a whole fleet, as long as there’s an ABN behind it.

Small and medium businesses: what providers look for

If you run a small or mid‑sized business, eligibility usually comes down to demonstrating that you’re a real trading entity that can meet its monthly fuel bill.

Typical criteria include:

- A valid ABN for a company, partnership, trust or sole trader

- At least a few months of trading history, sometimes more if you’re seeking higher limits

- A clean enough credit file or bank history for the limits requested

- Director or owner consent to the account and any personal guarantee if required

Different cards appeal to different fleet profiles:

- Single‑brand cards (Shell Card, BP Plus, AmpolCard, United Card, 7‑Eleven Fuel Card) suit businesses happy to mostly use one network.

- Multi‑brand cards (FleetCard, WEX Motorpass, some 7‑Eleven Fuel Pass products) suit fleets that roam widely and want to refuel almost anywhere.

As long as you meet the baseline eligibility, the real decision is less “can I get a card?” and more “which card makes the most sense for how we actually drive?”

Credit checks, prepaid options and “no credit” cards

One of the biggest question marks around eligibility is whether a fuel card will involve a full credit assessment. The answer depends on the product type.

For standard post‑paid business fuel cards:

- Providers usually run some form of credit or risk check, especially for new businesses or higher spend limits.

- They may ask for accounts, bank statements or trading history if they can’t verify enough info from your ABN and credit file alone.

Can you get a fuel card for personal use?

This is where expectations and reality collide. In Australia, traditional fuel cards are not set up as personal consumer products.

- You generally cannot get a business fuel card without an ABN, even if you drive a lot for personal reasons.

- Major cards like FleetCard, Shell Card, BP Plus, AmpolCard and United Card all explicitly require an ABN to apply.

- If you’re just looking to manage household fuel costs, your better options are: rewards credit cards, fuel‑brand apps with price locks and discounts, supermarket fuel dockets, or prepaid fuel products from specific brands.

Some government or concession schemes use the language of “fuel cards” for support programs, but these are separate to business fuel cards and have their own eligibility rules around pensions, concessions and location.

Documents you’ll usually need to prove eligibility

Once you’ve ticked the “am I eligible?” box, the rest is paperwork – and the more you have ready, the smoother approval tends to be.

Common requirements include:

- ABN details: ABN number, legal entity name, trading name and business address.

- Personal ID: Driver’s licence or other government ID for the owner, director or authorised signatory.

- Contact details: Email, phone and postal address for statements and cards.

- Financial information: Depending on the provider, this might be as light as a quick online check, or it may include bank statements and basic trading history, especially for brand‑new businesses.

Most applications are now completed online and can be approved quickly if your ABN and identity pass automated checks.

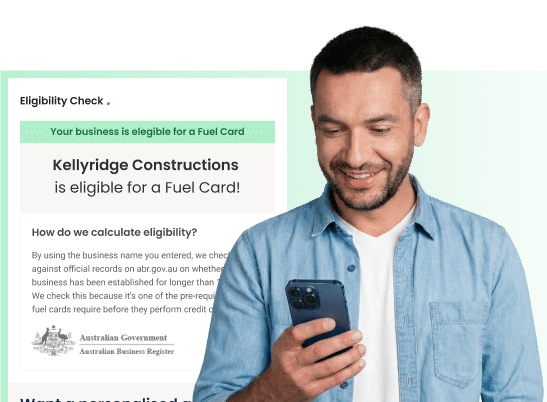

How to check your eligibility for a fuel card

Check your eligibility in a few clicks with Fuel Card Report’s free fuel card eligibility check and find the cards most likely to approve your business, and offer you the best discounts and card management fees.

FAQs

Can I have different limits on each fuel card?

Yes. Many providers let you set different spend caps, product restrictions or PIN rules per card, so high‑use vehicles and occasional drivers can be managed differently.

Do fuel cards work interstate or only in my home state?

Business fuel cards are generally national products. As long as the brand’s network operates in that state and the site is part of the program, you can usually use the card interstate.

Can multiple drivers share the same fuel card?

They can, but it’s not ideal. Most businesses issue one card per vehicle or per driver so transaction history is easier to track and misuse is easier to spot.

Can I use a fuel card to pay tolls or parking?

Some products allow limited non‑fuel vehicle expenses, but tolls and parking are often handled through separate accounts or tags. Always check your specific card’s allowed categories.

Do fuel cards integrate with accounting or fleet software?

Many modern fuel cards offer data exports or direct integrations (CSV, API or app‑based) so you can feed transactions into accounting, payroll or fleet‑management tools.

Can I temporarily suspend a card instead of cancelling it?

Yes, a lot of providers let you pause a card if a vehicle is off the road or a driver is on leave, then reactivate it later without issuing a brand‑new card.

Is there a maximum number of cards my business can have?

There usually isn’t a hard limit, but very large numbers of cards may trigger extra checks or require a more formal fleet agreement and tailored credit limit.

Can I change fuel card providers later if my needs change?

Absolutely. Businesses often switch when their fleet grows, routes change or they need different discounts or network coverage; just allow for a transition period where both systems overlap.

Enquire to save